As the property market heats up again, you may be interested in buying a new home and taking up a Sibor-pegged property loan.

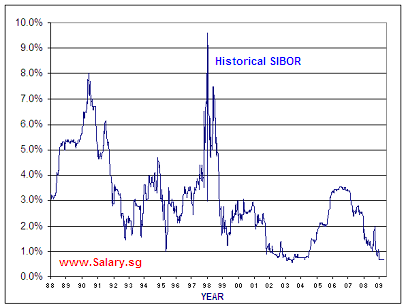

Do you know that the 3-month SIBOR rate shot up to an astonishing 9.5% in early 1998?

Or that it went to a low of 0.56% in mid-2003?

The following chart shows the interesting history of the 3-month Sibor rates:

Banks that offer Sibor-linked home loans include Stanchart, DBS and HSBC. Most of them use the 3-month Sibor, while some also provide a 12-month Sibor option.

Use this MAS tool to track the Sibor rate. The 3-month Sibor currently stands at 0.69%.

23 Comments

Property market is not hotting up. Its a temporary blip due to the increase in buying from the dramatic crash in the previous quarter.

Once this initial buying phase ends (and I believe it has), the prices will continue their fall.

Several reasons: excessive quantity, lack of jobs for both locals and expats.

no wonder my agent friends are looking for jobs. they say the buyers and sellers are simply unrealistic. one side asks for record low prices while the other side asks for the sky. in the end transactions are few and far between. it’s little wonder property ‘experts’ in the news are once again advising that property recovery is a long way to go and sellers better ask for realistic prices if they really want to sell.

Same thing with the rental market. Property owners continue to be unrealistic with their prices and the agents are making things worse by adding at least 25% on top. This is all psychology i.e. the 5 steps of mourning. Property owners have had it good over the last few years and can’t believe that the good times are pretty much over.

If sellers and landlords can afford to ask for better prices and if there are buyers and tenants willing to bite, why not?

To turn it around, I can also claim that it’s the buyers and renters who are unrealistic in their expectations.

Times have changed. You can no longer find noodles that cost $1 a bowl.

Exactly, the sentiments echo in the market. Landlord ask for sometime high and renter does not want to budge. So we will see if the landlord has more savings or the renter can live in his tent longer. But with more job losses coming, personally I fell that the landlord will have his saving deplicted sooner.

Don’t underestimate landlords. We are rich. 🙂 Let’s see if renters blink first.

landlords can still hold now that interest is low, buyers won’t bite if prices don’t lower, renters can still rent since rental is low, so actually nothing will happen…all sides will happily stay status quo…agents will hv to look for another job though

what’s happening now is oppotunistic buying to alleviate pent-up demand. once this is satisfied:

1. excess supply when more units get TOP in 2010

2. rental continue falling as more expats are sent home or have allowances slashed

3. developers lower prices to get sales

it’s unheard of for prices to rise in a recession

i’m keeping all my cash and cpf now, and will continue to pay low rent until prices are less outrageous

Still the worst is not hit the people much. Its just in the market and investers pocket. Don’t be tempt in the real estate now. This is not the bottom just one step free fall from the historic peak. It will slightly raise and then will crash.No more way to make easy money anywhere in the world. Be patient you are not going to miss the bus. If you take the bus know no could save you.

Pingback: Historical SIBOR (see graph) - Salary.sg Forums

Pingback: 2 Risks of Sibor-Pegged Home Loan | Salary.sg - Your Salary in Singapore

anyone know why did the sibor rate spike up to 9.5%? and what effect did it have on the property market?

it’s because of the asian currencies crisis when countries defend their currencies by raising rates or selling usd or both, net result is always high interest rates.

some people say it should not happen again, but never say never.

Well, you get quite a number of re-possesions happening them cos HL instaments easily doubled or more. When the banks repo they then proceed to sell off at thier reserve/minimum price to cut losses. (If you are a scrap hunter, you could wait for auctions)

97-98 was bad as you could almost get a full loan on your property when u bought in the 96 boom and the banks had to do some write-offs.

Effectively, a depressed property market for some time before all started picking up again only in 04-05…

the property market is holding up very well of late, economy seems to be picking up, and inflation seems rampant…. despite just barely being out of this recession…

seems like the scrap hunting days are kinda over…. property investors are alot more resilient than before.. more so after the rise in the equity market, and basically… everyone seems flushed with cash these days.

Inflation here we come…

with inflation comes interest rate increases (hypothesis 1). those who are saddled with loans will have trouble holding on.

some may think that high inflation will also push up ppty prices, but it’s actually the opposite – ppty prices will in fact come down because a lot of ppty units are financed with debt, and if hypothesis 1 comes true, the debtors will have trouble holding on and must sell down their units.

that is when bargain hunters come in.

never say this time it’s different. never say never. and don’t forget that we are in uncharted waters now – as agreed by central banks and economists all around the world.

So it would be prudent for one to opt for fixed interest rates on their housing loans rather than SIBOR pegged loans?

& would it be true to say that SIBOR will rise once there is a depressed property market?

What will be the order of the day with the govt releasing more land parcel?

Seeking advice on the above.

– the miserably newly married

if you’re newly married and combined income is less than 8k, why not get a hdb flat and get a hdb loan?

if i’m buying condo, i would pick a sibor-pegged loan since sibor is low now. if possible, i would try to keep the lock-in period short to allow for refinancing to take advantage of future good packages.

Unable due to total income just above the 8k cap. So we have to take bank loan. Thanks for the advice.

Since can afford only hdb, what other options should i cover? We aint cash rich.

have you considered buying EC? the cap is 10k.

Just above 8k can appeal to HDB. They will look at case-by-case basis.

Dear Admin, your link to the MAS Tool is no longer valid. New link is as follows: http://www.mas.gov.sg/data_room/msb/domestic_interest_rates.html

Corrected. Thanks, mate.